Traders often ask the question, “which market is better to trade, spot or futures?”.

The short answer is spot markets if you are looking to make longer-term investments. If you are hoping to hedge your trades or use increased leverage, you will want to trade the futures market.

I hope that is as a straightforward of an answer you can find anywhere on the web on the spot market vs futures market debate.

Now that I have addressed the answer for those of you with a 10-second attention span, let’s unpack this question further.

In this article, we will discuss six key differences between spot and futures markets. We will address questions such as does one market offer better access to pricing or trade execution?

However, before we dive deep, let’s first cover the basics of these markets.

Chapter 1: Overview of Spot and Futures Markets?

What is a Spot Market?

You may hear traders refer to the spot market as the cash market.

A spot market or cash market is where the exchange of financial instruments settle immediately. Stocks and currencies are the most well known spot market instruments.

Can you think of any spot markets? How about the Nasdaq for stock traders. If you trade currencies, Forex is another large global spot market.

A rule of thumb for spot markets is ownership of assets transfer immediately after a buy or sell transaction.

What is a Futures Market?

A futures market is where participants buy and sell contracts for delivery on a specified date in the future.

The futures markets include various instruments like commodities, stock indexes, currencies and select stocks.

Financial instruments on the futures markets are also known as derivatives, because the pricing of the contracts is based on the underlying security in the cash market.

For example, a Euro FX futures contract is based on the EUR USD spot forex price. Another example is the E-mini S&P 500 futures contract tracks the price of the S&P 500 index in the stock market.

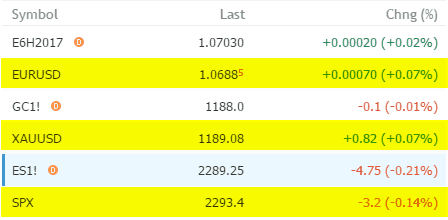

The table below illustrates examples of spot and futures market prices.

Spot and Futures Market prices

Notice there are minor price differences between the spot and futures markets highlighted in yellow.

Again, why the price difference?

Now that you are grounded on the two markets, we will shift our focus to the 6 key differences, which will help answer this question and more.

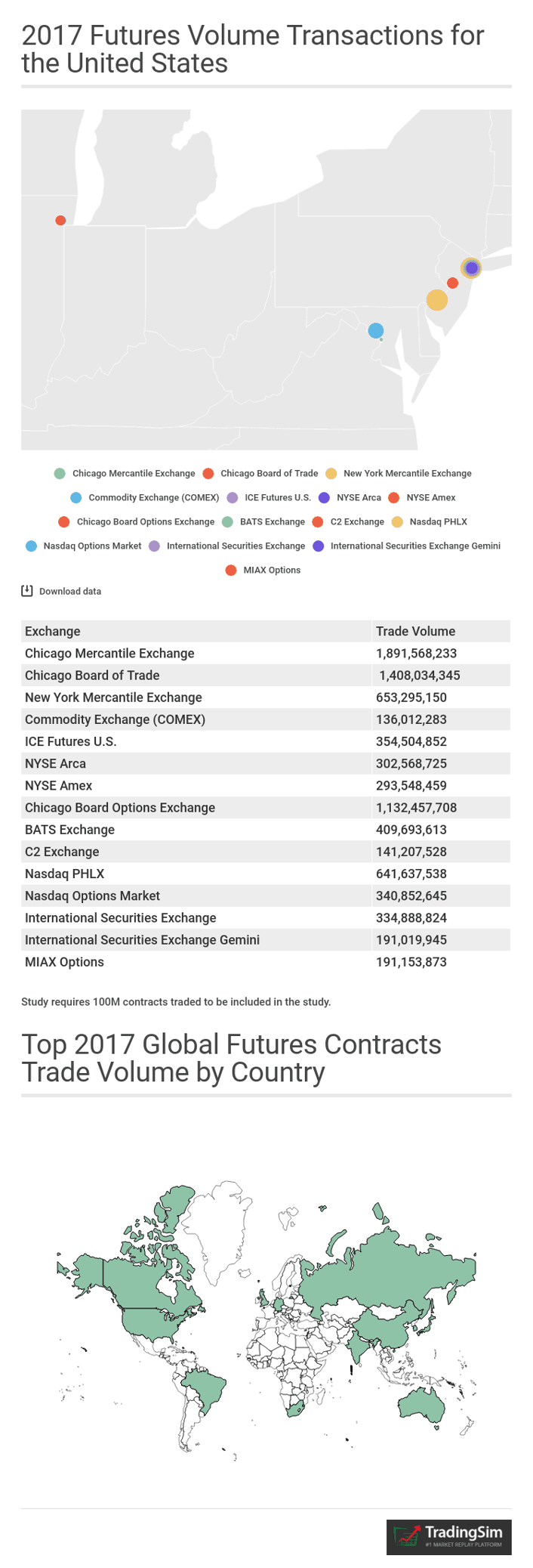

top futures exchanges

Data provided by FIA.

Chapter 2: 6 Key Differences Between Spot and Futures Markets

1. Counterparty Risk

Managing Counterparty Risk – Futures Markets

Counterparty is the process where there is a buyer and seller for each transaction. Since futures trades settle in the future, the last thing you want is to have no one on the other side of the trade.

Futures exchanges utilize two types of risk mitigation techniques to reduce the risk of this occuring: (1) performance bonds and (2) maintenance margin.

Performance Bond

To begin placing trades, you need a performance bond or initial margin. This essentially is the cash in your account to cover trade obligations.

Maintenance Margin

This maintenance requirement is the minimum amount of cash to cover all open positions.

The maintenance will differ based on your type of position (long/short), the specific requirement of the security you are trading and if you are holding the position overnight.

To touch upon more advanced methods used by the exchanges, let’s dive into when things go your way quickly and when you lose your shirt.

Price Moves Significantly In Your Favor

If price moves significantly in your favor, futures prices are marked-to-market, which means the profit is credited to your account from the maintenance margin.

Price Moves Sharply Against You

If a trade moves significantly against you, the difference is made up by deducting this amount from your maintenance margin.

When the maintenance margin falls below the initial margin, you are issued a margin call and required to fund your account to avoid liquidation.

This request to fulfill your obligations can come in the form of an automated email or a phone call if you have a sizable position.

Managing Counterparty Risk – Spot Markets

Margin in the spot market is an upfront fee with the broker and is not related to counterparty risk.

Is Counterparty Risk a Big Deal?

According to research conducted by the IMF, counterparty risk is largely dependent on the creditworthiness of the institution and its supporting casts of banks and broker dealers.

If you think managing counterparty risk is not a concern, think back to the mortgage crisis.

Essentially a lot of notes came due and there wasn’t money on the other side of the trade to complete the transaction for credit default swaps.

I think we all know how that played out.

2. Trade Settlement Period

Spot Market Settlement Period

For some spot markets, the allowable settlement time period is two working days.

While this is contradictory to the term “spot”, two working days are for the transfer of cash from the buyer to the seller.

However, in most cases, spot market prices settle near real-time.

This is most common with with spot Forex markets where transactions are sent electronically and settle immediately.

Futures Market Settlement Period

In the futures markets, the underlying asset has a specific settlement date in the future.

If you are long a futures contract, you agree to buy that contract on a specific date down the road.

Conversely, if you are short, you have entered an agreement to sell the contract on a future date.

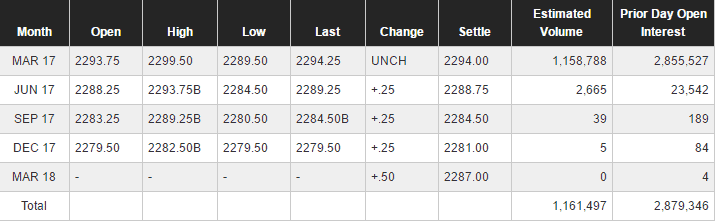

As you can see in the below table of the S&P E-mini contract, there are different expiration dates for each contract.

CME Futures, Contract Settlement Details

If you elect to not deliver the contracts on the specified date, you will need to roll your contracts to another out month.

Stocks do not rollover and you can hold them as long as the company is active on the respective exchange.

Therein lies the key difference between the two instruments – the element of time.

3. Hedging Against Risk

Traders use the futures market as a hedge against spot markets.

Why not the other way around?

Well, your ability to leverage is far greater in the futures market. Therefore you can purchase a few contracts, but able to hedge against a sizable spot market position.

This allows you to prevent any catastrophic move against you that could blow up your account, without risking a lot of your capital.

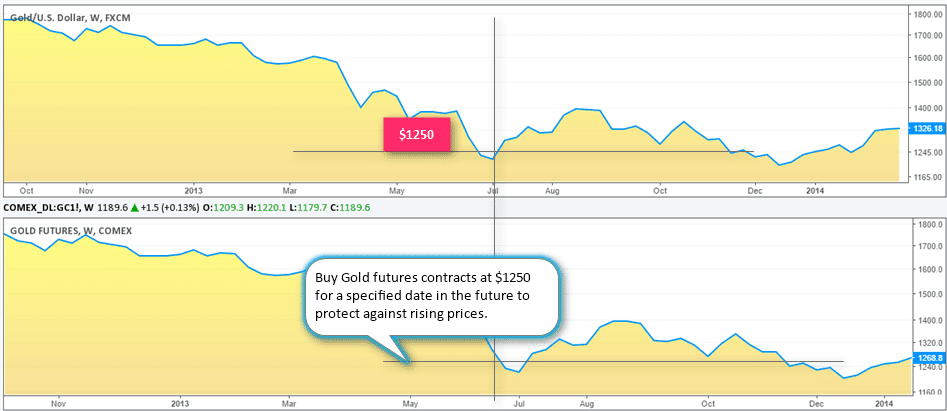

For example, if you had short exposure to the XAU/USD as depicted above, you could buy futures contracts to hedge against rising prices.

4. Futures are Best for Trading Commodities

History of Commodities Trading in the US

Although the futures markets today are made up of interest rates derivatives, Treasuries, and stock index futures; futures markets were originally known for trading commodities.

In the U.S. grains were one of the first commodities to trade in the early 1800’s and began as a forward contract.

In 1848, the Chicago Board of Trade (CBOT) exchange was formed where farmers and merchants could buy and sell commodities for cash.

The buying and selling process eventually evolved into contracts.

For nearly 100 years, agricultural products were the most commonly traded futures contracts, which slowly expanded to include other commodities such as soybeans in 1936 and cotton futures in 1940.

Precious metals began trading in the 1960’s and currency futures began to appear in the 70’s after the Bretton Woods agreement, where the U.S. dollar was depegged from gold.

Why Futures are Best for Trading Commodities

Seasons

Agriculture operate on a seasonal cycle that can impact the ability to grow and deliver these commodities.

Therefore, you need a way to hedge your trade and to take positions based on the target settlement date. This way if you think their will be a rain shortage, you can open a short position with a target settlement prior to the end of the drought.

Less Financial Exposure

You can purchase a large quantity of the commodity without opening a large cash position – see Chapter 6 for more details.

Pure Play

You are taking ownership of the actual commodity, versus owning a stock or ETF, which should mirror the derivative.

ETFs and stocks may not react the same way as the commodity, which is again time based.

Trade with the Crowd

Also, the majority of traders are interested in commodities trade on the CME and do not heavily invest in spot products that mirror the trade activity of the precious metal.

5. Futures prices are different from spot market prices

Futures prices are different because of carrying costs and carrying return

Although futures prices settle on a daily basis, marked-to-market, the price of the futures contracts differ from the underlying spot or cash market.

The cost of holding a futures contract include interests, financing costs, and storage costs to name a few.

Traders incur these expenses during the respective month they are trading.

Conversely, there are carrying returns which are dividends and bonuses paid out during the time the time you have ownership of the commodity contract.

Despite the differences in price of the futures and the spot markets, towards the contract’s expiration date, the futures price and the spot price tend to converge.

6. Ability to Leverage

A major difference between spot markets and futures markets is the concept of leverage.

While you can leverage some spot markets such as the Forex OTC, the way margin and leverage works in both these markets are very different.

In futures, every contract controls a specified amount of units of the underlying commodity or asset.

For example, a standard corn futures contract controls 5000 bushels of corn. Thus, if corn was trading at $7 a bushel, then one futures contract has a value of $35,000.

Another example of leverage is crude oil.

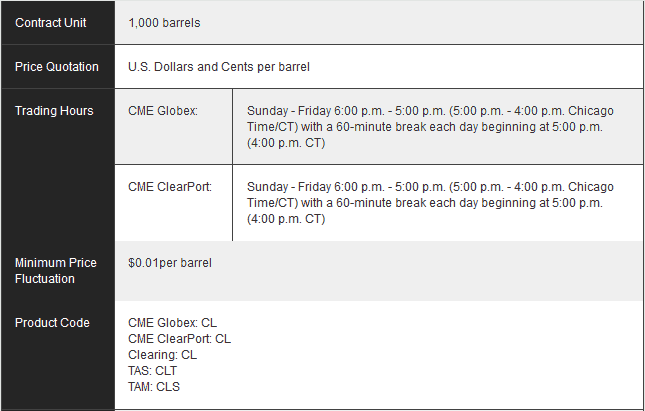

A standard crude oil futures contract controls 1000 barrels of oil. If the price of oil was $50 a barrel, then a standard futures contract would have a value of $50,000.

Crude oil futures contract leverage example

Trading futures requires you to post an initial margin also known as a performance bond.

This is the amount of money you must commit in order to take ownership of one contract.

Oil has an initial margin of $3,250, which translates to a margin requirement of approximately 15 to 1.

Generally speaking, the margin requirements for futures markets is much less than equities. For most cash exchanges, there is a 25% requirement.

The one spot market outlier is the Forex Exchange, where you can leverage 100 to 1.

In Summary

To conclude, the cash or OTC market are for traders that want to make buying and selling decisions irrespective of time.

The futures markets are for traders that want to hedge their exposure to an underlying market and still have the ability to make a great return.

Intro to Chart Patterns

Intro to Chart Patterns