Volatility is your friend when trading the market. It is like dark matter in the universe; you can’t see it, but it’s the very essence of the market. There are a number of volatility indicators, one of which we will cover in this article. Volatility is such a unique attribute, how do you know when it’s considered just right or a little over the top? To ignore volatility could be one of the most costly errors in your trading career. In this article we will decompose volatility and provide you a simple, yet effective way to start tracking this tool when trading.

There are a number of volatility indicators in the marketplace. None of which I plan on covering in this article. If you have been reading the Tradingsim blog you will quickly notice as you scan through the articles that I like to keep things simple. To that aim, we are only going to focus on one volatility indicator and that is the average true range (ATR). For those that have never heard of the average true range, it basically tracks the range of price movement in a security. In Lehman’s terms it looks at the spread between the high and low points of each day or time interval over “x” period of time. If the stock begins to swing wildly, then the average true range will increase in value. Conversely when things get a little choppy or quiet, the average true range will fall in value. The great thing about the average true range is it doesn’t provide oversold or overbought values. So, all of you people looking to get out of doing your own homework and analyzing the stock, I feel sorry for you.

There are probably a dozen or more indicators that provide what I am going to show you, but for my simplistic folks out there you will appreciate what I am getting ready to present. To perform this exercise you will need three things: (1) a chart, (2) average true range indicator and (3) a calculator. One thing you will notice is that the average true range can have any value because its based on the range of the stock. You could look at Apple and see an ATR value of 15 and then switch over to ZNGA and see a value of 2. On face value you really have no way of knowing which stock is more volatile than the other. You can look at the average true range values over the last number of bars to try and identify some sort of anomaly. Only problem with this approach is if you are scanning the market and looking through hundreds of charts, who has the time to perform not only a deep dive analysis of the chart, but also of each stock’s ATR? We need a quick way to analyze the volatility in order to make quick decisions.

If your charting application has the ATR indicator I want you to perform a very simple function. Take the ATR and divide it by the closing price of the stock. So, if the stock closed at $30 dollars and the ATR is at 3, then you would get a value of .1 (3/30). The higher this value the greater the volatility in the stock. Now what you need to do is look through your specific time frame (i.e. 1-min, 5-min, 15-min). Identify stocks that have the sort of volatility you are comfortable with and start to think of which manipulated ATR works best for your trading style. You will notice a “comfort” range will start to develop.

Let’s make this tangible, because I feel like I’m losing you. I like to trade breakouts in the morning and I need to make a minimum of 1.6% on every trade I take. So, if I buy a stock that trades tightly I am basically walking into that trade where the odds are against me making my profit target. This is where so many traders go wrong. If you do not read anything else in this article, please understand this basic principle, the volatility of the stock you are trading must be in direct alignment with your profit targets. If you can master this principle you will have control of the “dark” matter present in the market.

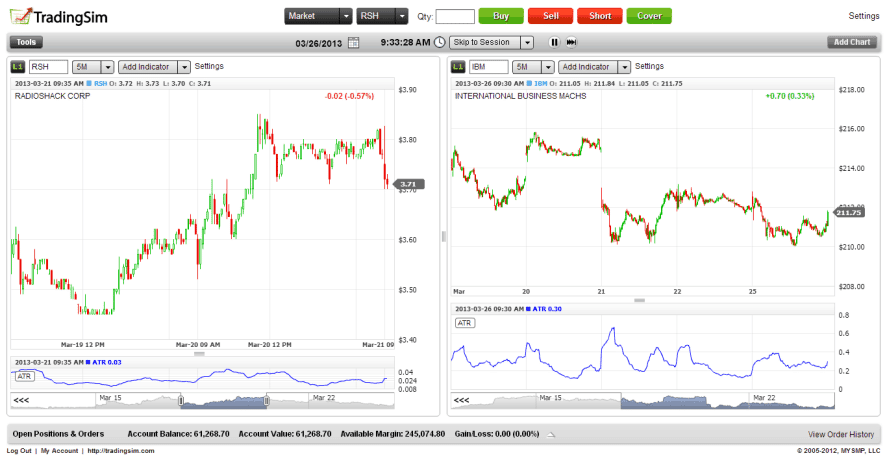

Let’s look at a real-life example of how we would apply this technique. Trader Susan is what what I like to describe as a real risk taker in the market. It does not phase her if a stock moves wildly in a matter of minutes. To Susan this is putting some skin in the game. As she scans the market Susan comes upon two charts. The one on the left is Radio Shack and the chart on the right is IBM.

Which of the two charts do you think Susan would want to trade? If you are honest with yourself the chart on the right appears to have wilder swings in it’s ATR. Well this would happen to be IBM. Now, upon further review when we perform our simple ATR calculation we get the following:

RSH: .04/3.82 = .010

IBM: .63/210.28= .003

Now what does this mean. Well this is telling you that in a head-to-head competition RSH is 3 times more volatile than IBM. Could you see that just looking at the candlesticks? Of course not. Depending on your zoom and the respective time frame, a stock can give the perception of being a mover. Well why did IBMs ATR appear to have a greater swing. The range on IBM is in dollars, while RSH is in pennies. Naturally the swings in the ATR will appear much larger for IBM and give the illusion the stock has far greater volatility.

In the modern day world we are very reluctant to place people and sometimes even things into buckets. Well, when it comes to classifying your stocks, you need to be pretty judgmental. First, you will want to determine what type of trade you are looking to place in terms of your appetite for volatility. This could be the same all day, everyday or your risk profile could change depending on the market. You will want to place yourself into 1 of 3 buckets: (1) low key, (2) middle of the road, and (3) looking for some action. Now since every time frame will present different values for the manipulated ATR and each trader will need to define what volatility means for their system, there are no predefined values. Sorry, you have to do a little work. Let me give you an example of how this is done so you have a blueprint.

I am a 5-minute trader; this is my permanent zip code. I also like to stay on the wild side of the “middle of the road” but not quite in the “looking for some action” crowd. After scanning the market I have noticed the following ranges for me on my 5-minute charts:

(1) Low Key = .001 > .005

(2) Middle of the Road = .005 > .01

(3) Looking for some action = >.01

Again, this is on the 5-minute chart, so my manipulated ATR values are going to be much smaller because the high/low range on the candlestick is smaller the lower the time frame you trade. If for example you were to use a 60-minute bar the starting ATR value would be much larger than a 5-minute candlestick and therefore your manipulated ATR value be considerably larger.

You can only ask of the market what she can bear. As a new trader I would put on positions and then get restless when things did not happen as smoothly as I was expecting. This was because what I thought would happen in 20 minutes hadn’t happened during the day for the stock in over 3 weeks. So, why would things change that I am in the trade? It’s not enough to identify a good setup, place your stops and follow all of your rules to the letter. You and the market have to be sync in terms of what you expect from each other.

Try placing the last 50 or so of your day trades into the three buckets. Watch how you will notice that on a good number of your losing trades or not so great trades, you were just asking too much from the market.

{kind=link}